We are a non-profit organisation, founded in 2005. Discover what we do, our governance bodies, team and more.What we do >Our Board of Directors >Our Team >Our partners >Work with us >

Members Directory >Additional Services >Become a member >NEW! The Governance Desk >

With +200 ILA members involved in 20 working committees, we keep our members up to date with regulation, hot topics on governance matters as well as upcoming trends.Our Working Committees >

Some ILA courses can be aggregated into broader Paths, which provide complete training on specific subjects.

Find out which training and e-learning are currently on offer.Upcoming courses E-learning

This professional qualification will grant you the title of ILA Certified Director.

This professional qualification will grant you the ILA Certification in Company Secretarial & Governance Practice (CGO Certification).

This professional qualification will grant you the title of Fund Governance Expert.

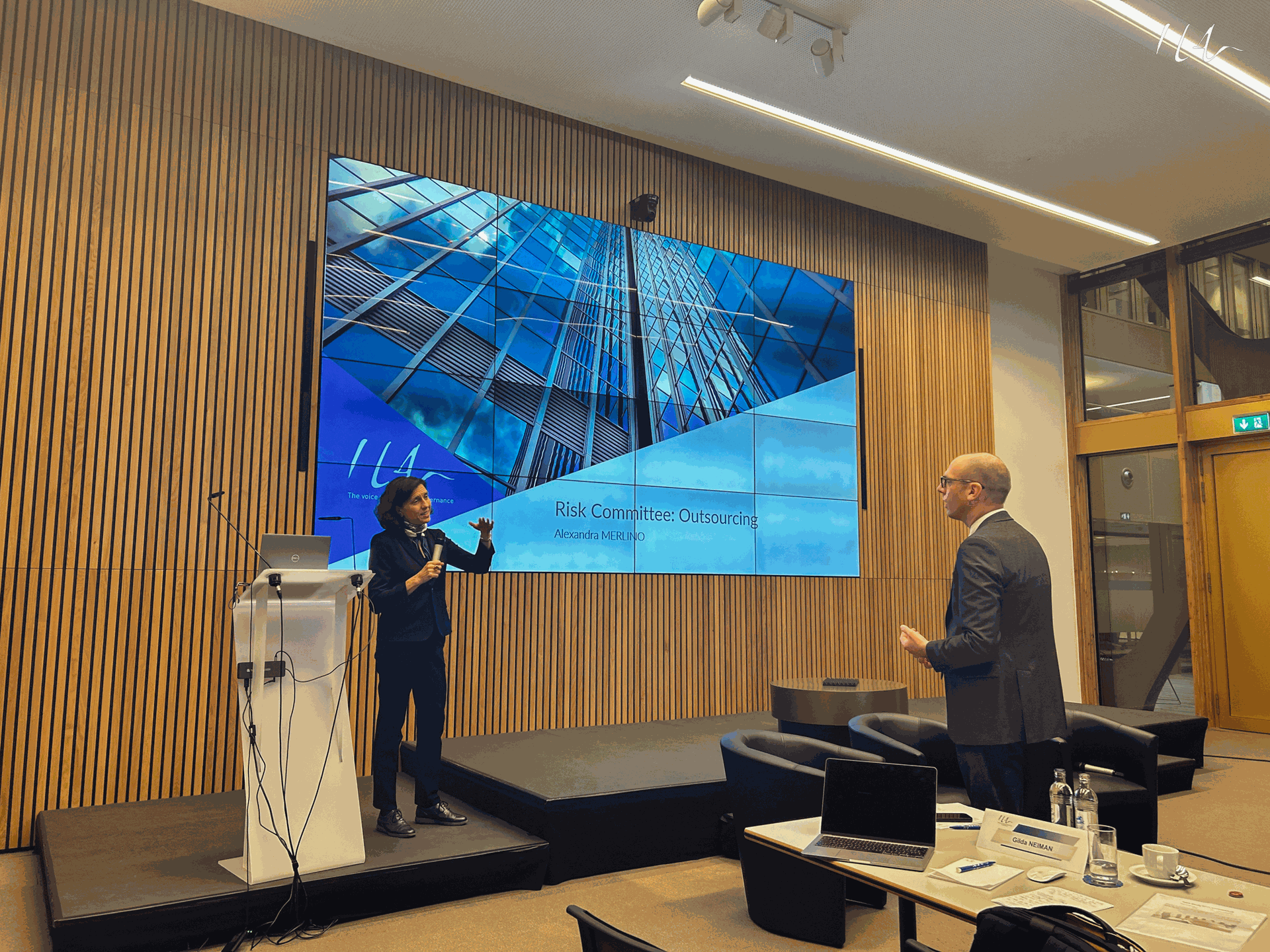

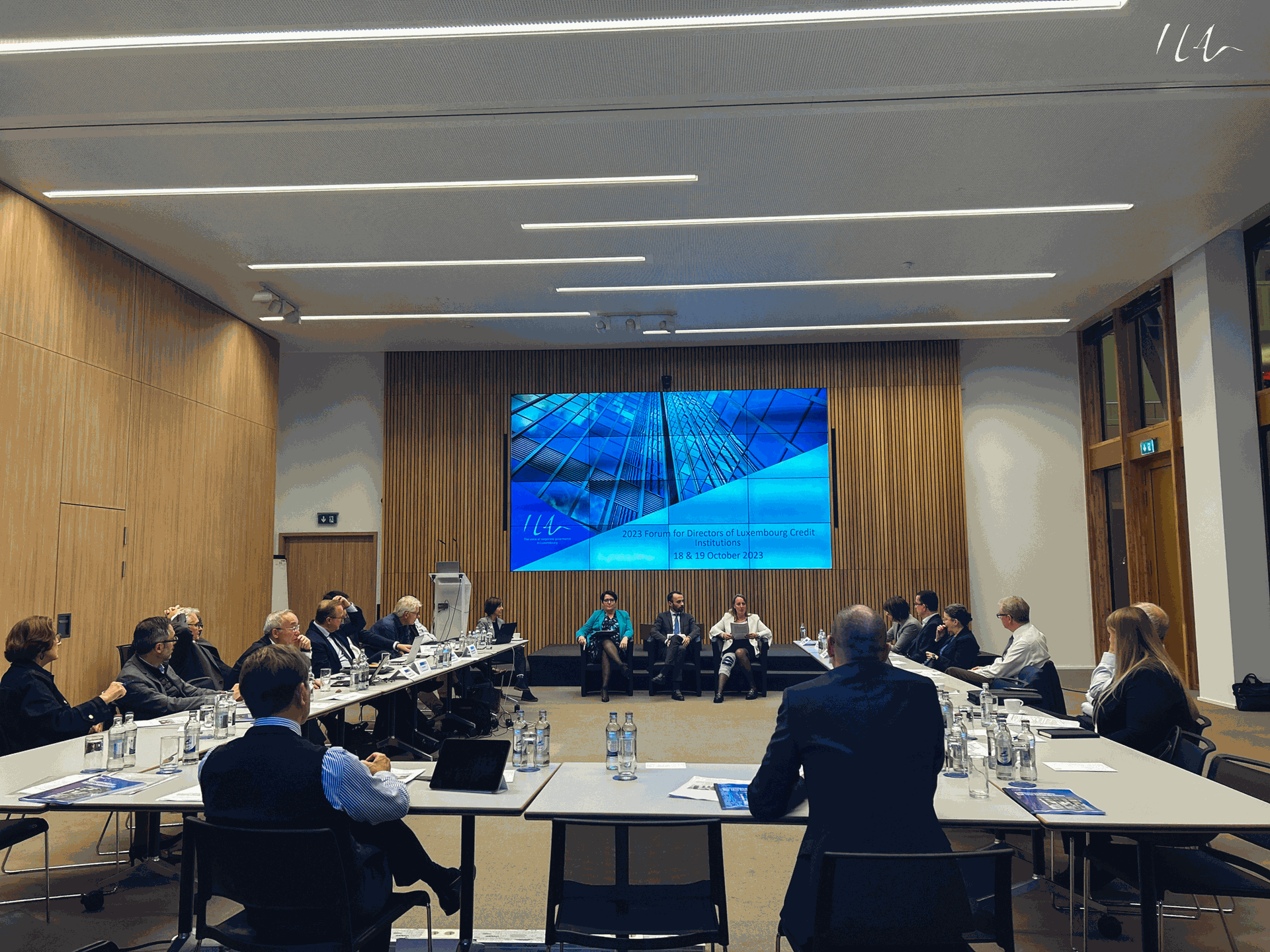

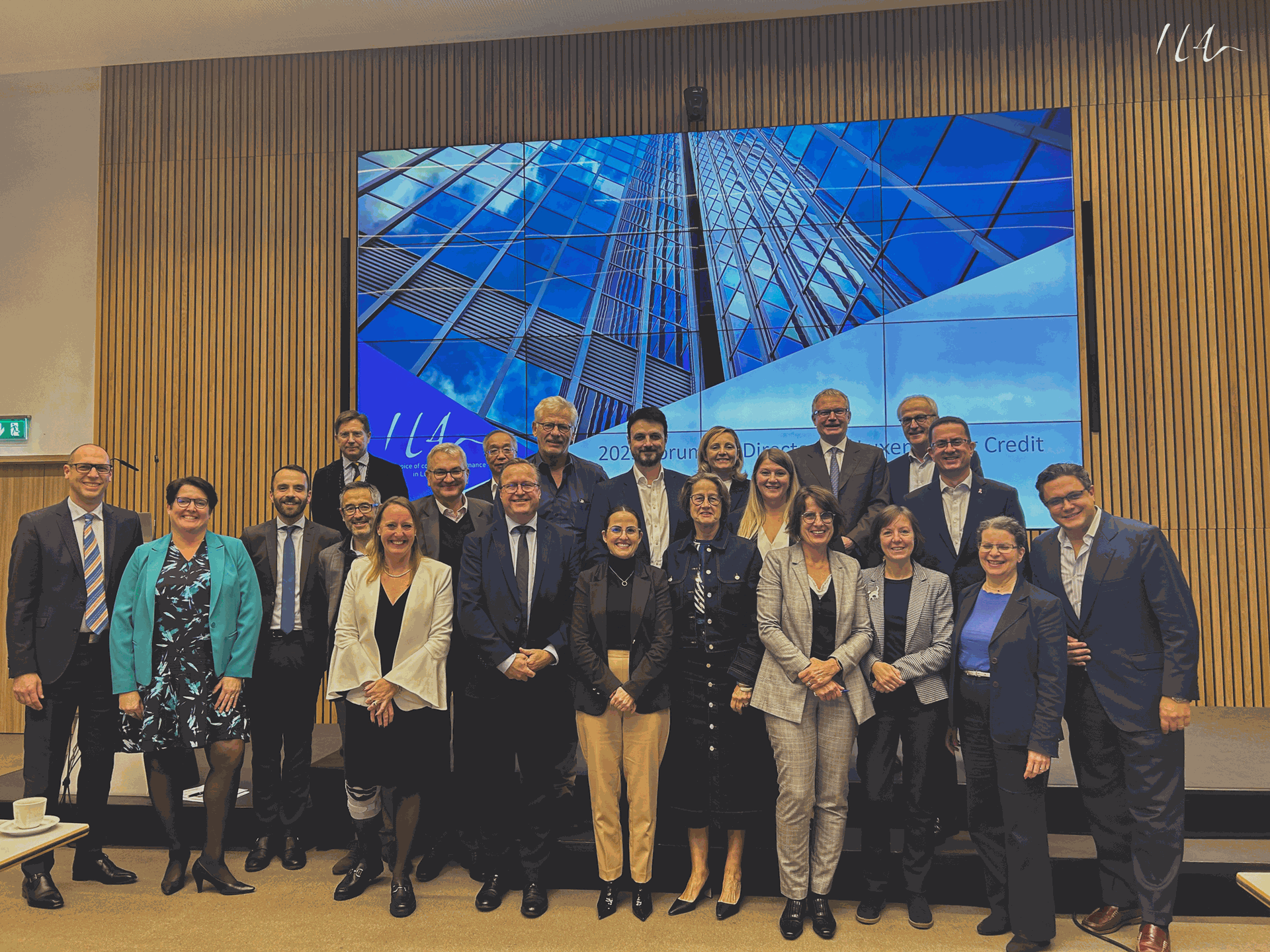

Here are the photos of the forum organised in October 2023: Forum for Directors of Luxembourg Credit Institutions.

We use cookies to provide you a better user experience.